As solar energy becomes more popular across the United States, many homeowners are exploring ways to install solar panels without paying the entire cost upfront. Two of the most common financing options are solar loans and solar leases. Both options allow homeowners to install solar panels with little or no upfront investment while reducing electricity bills. However, they work in very different ways and offer different financial benefits. Choosing between a solar loan and a solar lease depends on your financial goals, credit profile, and whether you want to own your solar system or simply pay for the electricity it generates. Understanding the differences between these two options can help homeowners make the best decision for their long-term energy savings.

What Is a Solar Loan?

A solar loan is a financing option that allows homeowners to borrow money to purchase a solar panel system. Instead of paying the entire installation cost upfront, homeowners make monthly payments over a set period, typically 10 to 20 years.

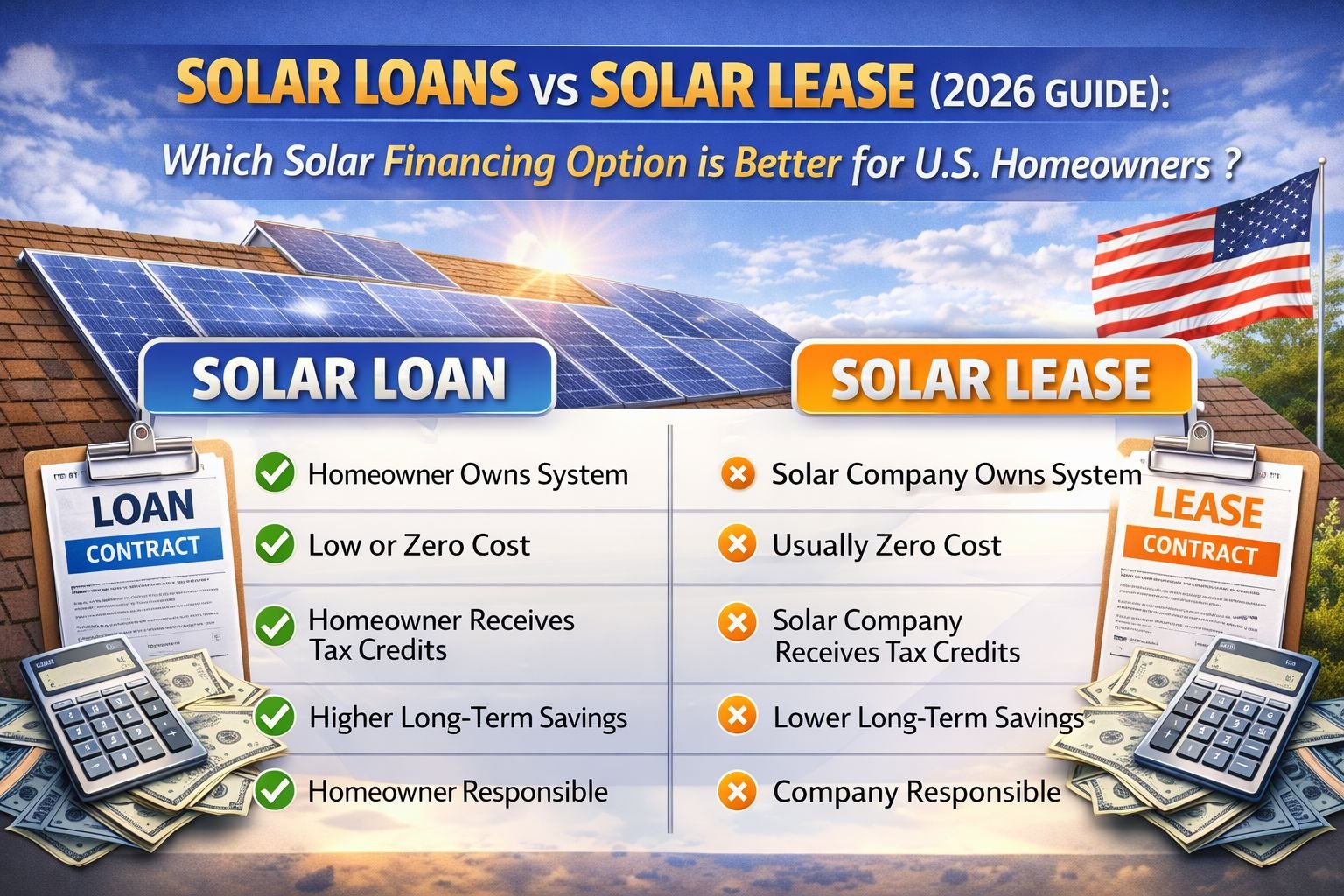

With a solar loan, the homeowner owns the solar system once the loan is paid off. Ownership means the homeowner can claim available incentives such as federal tax credits and benefit from the long-term savings generated by the system.

Typical Solar Loan Features

Solar loans usually offer flexible financing structures. Loan amounts can range from $1,000 to $100,000, depending on the size of the solar installation.

Interest rates vary depending on credit score and lender. Many solar loans offer rates between 4% and 17% APR, although highly qualified borrowers may receive lower rates.

Loan terms generally range from 7 to 25 years, with longer terms resulting in lower monthly payments but higher overall interest costs.

Advantages of Solar Loans

Solar loans offer several benefits for homeowners who want to invest in renewable energy. Because the homeowner owns the solar system, they can receive federal tax incentives and other solar rebates. Ownership also increases property value because the solar system becomes part of the home. In addition, once the loan is paid off, homeowners can enjoy decades of nearly free electricity. Solar panels typically last 25 to 30 years, which means many years of energy savings after the loan is repaid.

Disadvantages of Solar Loans

Despite their advantages, solar loans also have potential drawbacks. Borrowers must qualify for financing, which usually requires a good credit score. Monthly loan payments may also be higher during the early years compared to a solar lease. In addition, homeowners are responsible for system maintenance and repairs after the warranty period ends.

What Is a Solar Lease?

A solar lease is another popular way to install solar panels without paying the upfront cost. Under a solar lease agreement, a solar company installs the solar panels on the homeowner’s roof and retains ownership of the system. The homeowner pays a fixed monthly fee to use the solar energy produced by the system.

Most solar leases last 20 to 25 years, which is similar to the lifespan of solar panels.

How Solar Leases Work

With a solar lease, the solar company handles installation, monitoring, maintenance, and repairs. Homeowners simply pay a monthly lease payment to use the electricity generated by the system. Many leases require little or no upfront cost, which makes solar energy accessible for households that cannot afford the initial installation cost.

Advantages of Solar Leasing

One of the biggest advantages of solar leasing is the ability to install solar panels with minimal upfront investment. Maintenance and repairs are usually handled by the solar company, reducing responsibility for the homeowner. Lease payments are typically lower than traditional electricity bills, allowing homeowners to save money immediately.

Disadvantages of Solar Leasing

The main disadvantage of solar leasing is that the homeowner does not own the solar system. Because the solar company owns the equipment, the company receives the federal tax credits and other incentives instead of the homeowner. Long-term savings may also be lower compared to owning the system through a solar loan.

In addition, solar leases can complicate home sales because the lease contract may need to be transferred to the new homeowner.

Solar Loan vs Solar Lease: Key Differences

| Feature | Solar Loan | Solar Lease |

|---|---|---|

| Ownership | Homeowner owns system | Solar company owns system |

| Upfront cost | Often low or zero | Usually zero |

| Tax incentives | Homeowner receives incentives | Solar company receives incentives |

| Monthly payments | Loan repayment | Lease payment |

| Long-term savings | Higher | Lower |

| Maintenance | Homeowner responsibility | Company responsibility |

Long-Term Financial Comparison

Financial experts often note that purchasing a solar system through a loan typically provides greater long-term savings compared to leasing. Buying or financing solar panels allows homeowners to capture the full financial value of the system over its lifetime.

Although leasing may provide short-term convenience and immediate savings, homeowners who finance their system through a loan can benefit from lower electricity costs for decades after the loan is paid off.

Which Option Is Best for U.S. Homeowners?

The best option depends on the homeowner’s financial situation and long-term goals. Solar loans are often ideal for homeowners who want to maximize long-term savings and take advantage of government incentives. Leasing may be a good choice for homeowners who prefer a simple solution with no upfront investment and minimal maintenance responsibilities.

For homeowners planning to stay in their home for many years, owning the solar system usually provides the greatest financial benefit. However, leasing may be a practical option for households that want immediate energy savings without taking on debt.

Final Thoughts

Both solar loans and solar leases provide pathways for homeowners to adopt solar energy without paying the entire installation cost upfront. Solar loans allow homeowners to own their system and enjoy greater long-term savings, while solar leases offer a simpler option with little upfront investment and minimal maintenance responsibilities. Ultimately, the best choice depends on personal financial goals, credit profile, and how long the homeowner plans to stay in the property. By comparing both options carefully, homeowners can choose the financing method that best fits their energy needs and financial plans.